Financial aid awards are often confusing. I believe many colleges and universities intentionally make financial aid awards hard to decipher to trick families into thinking that their institutions are being generous even when they aren’t.

Obfuscation is an effective way to keep parents off balance.

Since we are heading into the season when students will be receiving their financial aid letters, I wanted to take a look at this critical part of the college admission process.

What Every Financial Aid Letter Should Contain

Here is what a good financial aid letter should contain:

- Full cost of attendance. This should be broken down into such expenses as tuition, room and board, textbooks and travel.

- Grants and scholarships.

- Types and amounts of loans. The loans should include the interest rates.

- Net amount student will have to pay after financial aid is deducted.

- Parent and student’s Expected Family Contribution.

Most financial aid letters don’t include all these elements, which truly is an outrage. If you find a financial aid letter incomplete, you should contact the school and get the missing information.

Check the EFC

I want to especially encourage you to obtain your Expected Family Contribution from the college.

Your EFC is what the financial aid formula says your household should be able to pay for one year of college. If the EFC isn’t provided and it usually isn’t, you YOU CANNOT DETERMINE if the award is a fair one or not.

If you need it, here’s a quick background on what an EFC is:

Your First Financial Aid Step

I am going to use a financial letter that a parent gave me last year from Pace University that illustrates why knowing an EFC is critical when evaluating an award letter:

What’s Inside This Letter

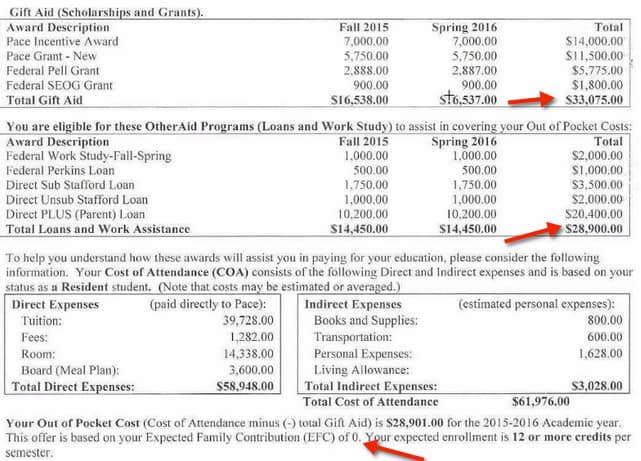

When I first saw this letter I thought Pace University had not included this family’s EFC in the letter, but I later saw that it was at the very bottom of the award without including an explanation. (See bottom red arrow.) It would have been very easy for the parents and the student not to know what this number was or why it was so important.

Before I share what the significance of this figure is, let’s take a look at what Pace was offering and not offering.

Gift aid. Pace gave this student $33,075 in grants and scholarships. In the award, $7,575 of this assistance came from the federal government (Pell and SEOG grants).

Loans and work study. After the gift aid was deducted, this student would have been expected to pay $28,900 for one year of college since the total cost of attendance was $61,976.

The Lowest EFC Possible

Was this is a good award?

You might think so since $33,075 sure looks like a lot of free money. But in reality, this is a terrible award. The reason why I know this is because the aid letter includes the family’s EFC.

This student’s EFC is $0. This means, according to the formula, that she has the financial ability to pay $0 for college. Students get an automatic EFC when their adjusted gross income is $24,000 or less.

Pace was asking this impoverished student to pay $28,900 for one year of school. Clearly that would have been financial suicide for this low-income family to take out loans to cover this cost.

In contrast, someone with a higher EFC could have been thrilled with this type of assistance.

Let’s say a wealthy student with an EFC of $60,000 applied to Pace and got a merit award of $25,000 a year. Thanks to the merit award, the student would be paying far less than what his or her household EFC suggests the family could pay.

Bottom Line:

When a financial aid letter is incomplete, make sure you get all the information you need before making any decision about where your child will attend college and what you can afford.

This was super helpful!

I wish someone had explained it like this before I went.

Thank you!

-Kay

Hi Lynn!

I just wanted to give you a heads up that I included your article in an article roundup for April.

You can find it here:

http://www.smartstudentsecrets.com/april2017kaysstudyroundup/

Keep in touch!

-Kay

Author

Thanks Kay, I appreciate it!

Lynn O.